计量经济学实验报告.docx

计量经济学实验报告.docx

- 文档编号:7989799

- 上传时间:2023-05-12

- 格式:DOCX

- 页数:24

- 大小:68KB

计量经济学实验报告.docx

《计量经济学实验报告.docx》由会员分享,可在线阅读,更多相关《计量经济学实验报告.docx(24页珍藏版)》请在冰点文库上搜索。

计量经济学实验报告

计量经济学实验报告

专业国际经济与贸易班级一班姓名姜祥丽学号20114913

实验一

(1)YY和GDP1的回归

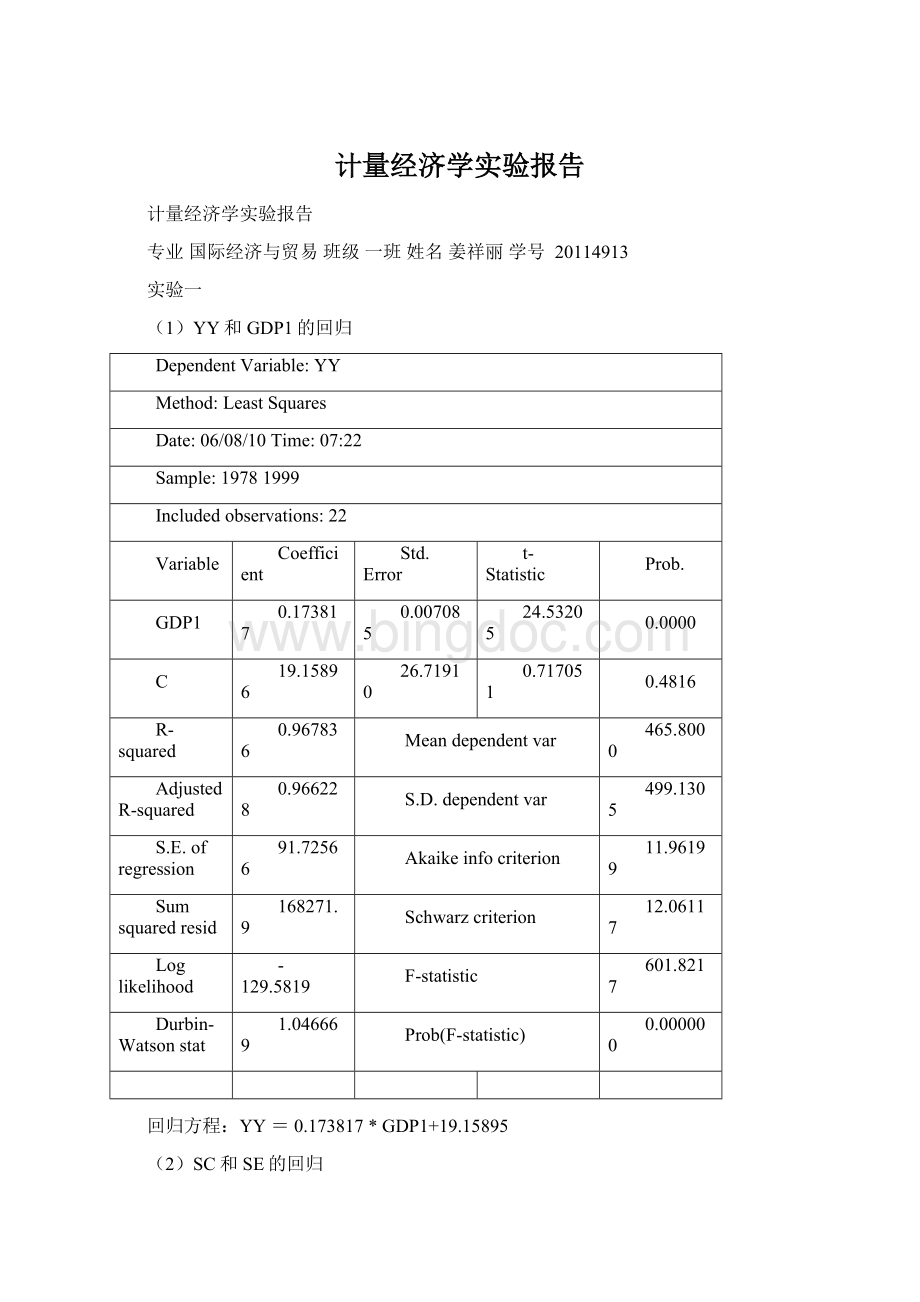

DependentVariable:

YY

Method:

LeastSquares

Date:

06/08/10Time:

07:

22

Sample:

19781999

Includedobservations:

22

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP1

0.173817

0.007085

24.53205

0.0000

C

19.15896

26.71910

0.717051

0.4816

R-squared

0.967836

Meandependentvar

465.8000

AdjustedR-squared

0.966228

S.D.dependentvar

499.1305

S.E.ofregression

91.72566

Akaikeinfocriterion

11.96199

Sumsquaredresid

168271.9

Schwarzcriterion

12.06117

Loglikelihood

-129.5819

F-statistic

601.8217

Durbin-Watsonstat

1.046669

Prob(F-statistic)

0.000000

回归方程:

YY=0.173817*GDP1+19.15895

(2)SC和SE的回归

DependentVariable:

CS

Method:

LeastSquares

Date:

06/08/10Time:

07:

27

Sample:

19781999

Includedobservations:

22

Variable

Coefficient

Std.Error

t-Statistic

Prob.

SE

0.482249

0.016112

29.93042

0.0000

C

31.03074

9.401733

3.300534

0.0036

R-squared

0.978162

Meandependentvar

215.8573

AdjustedR-squared

0.977070

S.D.dependentvar

219.5927

S.E.ofregression

33.25218

Akaikeinfocriterion

9.932625

Sumsquaredresid

22114.15

Schwarzcriterion

10.03181

Loglikelihood

-107.2589

F-statistic

895.8303

Durbin-Watsonstat

1.274578

Prob(F-statistic)

0.000000

回归方程:

CS=31.03074+0.482249*SE

实验二

(一)REV=-5826.158+0.084781035*GDP

(2517.475)(0.003311)

(-2.314286)(25.60453)

R2=0.976176SE=7732.823

DependentVariable:

REV

Method:

LeastSquares

Date:

06/08/10Time:

08:

04

Sample:

19781995

Includedobservations:

18

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP

0.084781

0.003311

25.60453

0.0000

C

-5826.158

2517.475

-2.314286

0.0343

R-squared

0.976176

Meandependentvar

38637.72

AdjustedR-squared

0.974687

S.D.dependentvar

48603.38

S.E.ofregression

7732.823

Akaikeinfocriterion

20.84877

Sumsquaredresid

9.57E+08

Schwarzcriterion

20.94771

Loglikelihood

-185.6390

F-statistic

655.5922

Durbin-Watsonstat

0.335513

Prob(F-statistic)

0.000000

经济意义检验:

财政收人REV对国内生产总值GDP的回归系数为0.084781,无论从参数的符合和大小来说都符合经济理论。

说明国内生产总值GDP增加1个单位,财政收人REV增加0.085个单位。

统计检验:

根据数据的统计方程,判定系数R2接近1,拟合优度较高;参数显著性t检验拒绝犯错的概率为0,即拒绝原假设,通过t检验,GDP对REV有显著性影响。

常数C的t检验的概率为0.034小于0.05,所以通过t检验。

(二)EXB=(-2457.310)+(0.719308)*REV

(680.5738)(0.011153)

(-3.610644)(64.49707)

R2=0.996168SE=2234.939

DependentVariable:

EXB

Method:

LeastSquares

Date:

06/08/10Time:

07:

44

Sample:

19781995

Includedobservations:

18

Variable

Coefficient

Std.Error

t-Statistic

Prob.

REV

0.719308

0.011153

64.49707

0.0000

C

-2457.310

680.5738

-3.610644

0.0023

R-squared

0.996168

Meandependentvar

25335.11

AdjustedR-squared

0.995929

S.D.dependentvar

35027.97

S.E.ofregression

2234.939

Akaikeinfocriterion

18.36626

Sumsquaredresid

79919268

Schwarzcriterion

18.46519

Loglikelihood

-163.2963

F-statistic

4159.872

Durbin-Watsonstat

2.181183

Prob(F-statistic)

0.000000

经济意义检验:

财政支出EXB对财政收入REV的回归系数为0.719308,无论从参数的符合和大小来说都符合经济理论。

说明财政收人REV增加1个单位,财政支出EXB平均增加0.72个单位。

统计检验:

根据数据的统计方程,判定系数R2接近1,拟合优度较高;参数显著性t检验拒绝犯错的概率为0,即拒绝原假设,通过t检验,REV对EXB有显著性影响。

常数C的t检验的概率为0.0023小于0.05,所以通过t检验。

(三)SLC=(-2411.361)+(0.431827)*GDP

(3076.237)(0.004046)

(-0.783857)(106.7267)

R2=0.998597SE=9449.149

DependentVariable:

SLC

Method:

LeastSquares

Date:

06/08/10Time:

08:

05

Sample:

19781995

Includedobservations:

18

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP

0.431827

0.004046

106.7267

0.0000

C

-2411.361

3076.237

-0.783867

0.4446

R-squared

0.998597

Meandependentvar

224062.6

AdjustedR-squared

0.998510

S.D.dependentvar

244763.3

S.E.ofregression

9449.149

Akaikeinfocriterion

21.24968

Sumsquaredresid

1.43E+09

Schwarzcriterion

21.34861

Loglikelihood

-189.2471

F-statistic

11390.59

Durbin-Watsonstat

1.715091

Prob(F-statistic)

0.000000

经济意义检验:

社会消费品零售额SLC对国内生产总值GDP的回归系数为0.431827,无论从参数的符合和大小来说都符合经济理论。

说明国内生成总值GDP增加1个单位,社会消费品零售额SLC分别平均增加0.432个单位。

统计检验:

根据数据的统计方程,判定系数R2接近1,拟合优度较高;参数显著性t检验拒绝犯错的概率为0,即拒绝原假设,通过t检验,GDP对SLC有显著性影响。

常数C的t检验的概率为0.4446大于0.05,所以没有通过t检验。

实验三

(一)把ZJ作为应变量,GDP1和T作为两个解释变量进行二元线性回归分析。

1、分别做ZJ和GDP1、ZJ和T的散点图:

分析:

从散点图看,变量之间不一定呈现线性关系

2、多元线性回归

DependentVariable:

ZJ

Method:

LeastSquares

Date:

03/31/13Time:

18:

40

Sample:

19781999

Includedobservations:

22

Variable

Coefficient

Std.Error

t-Statistic

Prob.

T

-6.728731

1.235938

-5.444229

0.0000

GDP1

0.176471

0.004305

40.99647

0.0000

R-squared

0.995817

Meandependentvar

378.1314

AdjustedR-squared

0.995608

S.D.dependentvar

458.5207

S.E.ofregression

30.38617

Akaikeinfocriterion

9.752360

Sumsquaredresid

18466.38

Schwarzcriterion

9.851546

Loglikelihood

-105.2760

F-statistic

4761.733

Durbin-Watsonstat

0.848685

Prob(F-statistic)

0.000000

得到估计方程为:

ZJ=0.17647447*GDP1+6.7287292*T

分析:

估计方程的调整判定系数为0.995608接近于1,所以拟合优度较高;方程显著性F检验拒绝犯错的概率为0,说明拒绝原假设,即方程显著性F检验显著;参数显著性t检验拒绝犯错的概率都为0,即拒绝原假设,通过t检验。

(二)把SE作为应变量,GDP1和T作为两个解释变量进行二元线性回归分析。

1、分别做SE与GDP1、SE与T的散点图:

分析:

从散点图看,变量之间不一定呈现线性关系

2、多元线性回归

DependentVariable:

SE

Method:

LeastSquares

Date:

03/31/13Time:

18:

03

Sample:

19781999

Includedobservations:

22

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP1

0.169558

0.002925

57.97489

0.0000

T

-4.712952

0.839743

-5.612372

0.0000

R-squared

0.997998

Meandependentvar

383.2595

AdjustedR-squared

0.997898

S.D.dependentvar

450.3519

S.E.ofregression

20.64551

Akaikeinfocriterion

8.979381

Sumsquaredresid

8524.746

Schwarzcriterion

9.078567

Loglikelihood

-96.77319

F-statistic

9972.446

Durbin-Watsonstat

0.566752

Prob(F-statistic)

0.000000

得到估计方程为:

SE=0.16955751*GDP1+4.7129508*T

分析:

估计方程的调整判定系数为0.997898接近于1,所以拟合优度较高;方程显著性F检验拒绝犯错的概率为0,说明拒绝原假设,即方程显著性F检验显著;参数显著性t检验拒绝犯错的概率都为0,即拒绝原假设,通过t检验。

实验四

要求一:

做ZJ对GDP1和T回归的残差趋势图和残差散点图。

结论:

从图上看ZJ对GDP1、T回归的残差存在异方差。

要求二:

做对ZJ和GDP1回归的Glejser检验。

(1)abs(e1)与GDP1做回归

DependentVariable:

ABS(E1)

Method:

LeastSquares

Date:

06/22/10Time:

08:

00

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP1

0.004387

0.001443

3.040305

0.0062

C

20.71896

6.063898

3.416773

0.0026

R-squared

0.305635

Meandependentvar

33.34424

AdjustedR-squared

0.272570

S.D.dependentvar

24.84736

S.E.ofregression

21.19219

Akaikeinfocriterion

9.028084

Sumsquaredresid

9431.287

Schwarzcriterion

9.126822

Loglikelihood

-101.8230

F-statistic

9.243454

Durbin-Watsonstat

1.148496

Prob(F-statistic)

0.006221

从F检验来看整个模型显著

(2)abs(e1)与GDP1^2做回归

DependentVariable:

ABS(E1)

Method:

LeastSquares

Date:

06/22/10Time:

08:

02

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP1^2

4.82E-07

1.64E-07

2.928548

0.0080

C

24.83660

5.329758

4.659985

0.0001

R-squared

0.289974

Meandependentvar

33.34424

AdjustedR-squared

0.256164

S.D.dependentvar

24.84736

S.E.ofregression

21.42984

Akaikeinfocriterion

9.050387

Sumsquaredresid

9643.999

Schwarzcriterion

9.149126

Loglikelihood

-102.0794

F-statistic

8.576393

Durbin-Watsonstat

1.132628

Prob(F-statistic)

0.008028

从F检验来看整个模型显著

(3)abs(e1)与SQR(GDP1)做回归

DependentVariable:

ABS(E1)

Method:

LeastSquares

Date:

06/22/10Time:

08:

03

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

SQR(GDP1)

0.464073

0.158455

2.928736

0.0080

C

12.16515

8.500612

1.431091

0.1671

R-squared

0.290001

Meandependentvar

33.34424

AdjustedR-squared

0.256191

S.D.dependentvar

24.84736

S.E.ofregression

21.42944

Akaikeinfocriterion

9.050350

Sumsquaredresid

9643.639

Schwarzcriterion

9.149088

Loglikelihood

-102.0790

F-statistic

8.577497

Durbin-Watsonstat

1.118705

Prob(F-statistic)

0.008024

常数项不显著,去掉常数项再进行回归得结果为:

DependentVariable:

ABS(E1)

Method:

LeastSquares

Date:

06/22/10Time:

08:

08

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

SQR(GDP1)

0.656981

0.085253

7.706276

0.0000

R-squared

0.220758

Meandependentvar

33.34424

AdjustedR-squared

0.220758

S.D.dependentvar

24.84736

S.E.ofregression

21.93392

Akaikeinfocriterion

9.056451

Sumsquaredresid

10584.13

Schwarzcriterion

9.105820

Loglikelihood

-103.1492

Durbin-Watsonstat

1.019181

(4)abs(e1)与1/GDP1做回归

DependentVariable:

ABS(E1)

Method:

LeastSquares

Date:

06/22/10Time:

08:

04

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

1/GDP1

-3994.363

3218.612

-1.241020

0.2283

C

39.30882

7.021346

5.598474

0.0000

R-squared

0.068328

Meandependentvar

33.34424

AdjustedR-squared

0.023963

S.D.dependentvar

24.84736

S.E.ofregression

24.54784

Akaikeinfocriterion

9.322066

Sumsquaredresid

12654.53

Schwarzcriterion

9.420805

Loglikelihood

-105.2038

F-statistic

1.540131

Durbin-Watsonstat

0.869730

Prob(F-statistic)

0.228283

从F检验来看整个模型不显著

从四个回归的结果看,回归(4)不显著,

(1)

(2)(3)显著,比较

(1)

(2)与(3)不带常数项的回归,还是选择

(1),方程为:

ABS(resid)=0.004387GDP1+20.71896

所以异方差的形式为:

σi2=σ2(GDP1)2

要求三:

已知ZJ对GDP1回归异方差的形式为:

把

作为权数来进行加权最小二乘法。

得到回归结果为:

DependentVariable:

ZJ

Method:

LeastSquares

Date:

06/22/10Time:

08:

24

Sample:

19782000

Includedobservations:

23

Weightingseries:

1/(GDP1^(1/6))

Variable

Coefficient

Std.Error

t-Statistic

Prob.

GDP1

0.162521

0.002949

55.11028

0.0000

C

-31.09968

9.069704

-3.428963

0.0025

WeightedStatistics

R-squared

0.990759

Meandependentvar

339.9230

AdjustedR-squared

0.990319

S.D.dependentva

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 计量 经济学 实验 报告

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《d t n l》公开课教案优秀教学设计5.docx

《d t n l》公开课教案优秀教学设计5.docx

-

《大禹治水》公开课教案优秀教学设计14.docx

-

《父与子》读后感10篇.docx

-

《红星美凯龙物业管理部安全操作手册》.docx

-

《白杨》公开课教案和教学反思.docx

-

《动物临床诊疗技术》课程标准.docx

-

《广州市建设工程监理合同》SF0206.docx

-

《安全系统工程第三版徐志胜版》课后答案.docx

-

《动画运动规律》课程教案模板.docx

-

《管理学原理》综合测验考试复习资料.docx

-

《计算机网络》实验指导书修改版.docx

-

《平行四边形的面积》教学设计8.docx

-

《生药学》课程指导书.docx

-

《闻一多先生的说和做》阅读练习含答案.docx

-

《易经系辞》通讲二十七.docx

-

《坐井观天》教学实录与评析教案文档资料.docx

-

《悲歌行》.docx

-

《窦娥冤》导学案.docx

-

《广州市商品房买卖合同预售示范文本》SF0102.docx

-

《计算机应用基础》练习题含答案.docx

-

《企业信息管理》形成性作业有答案版.docx

-

《食品安全法》试题答案.docx

-

《我的母亲》课后练习题答案.docx

-

《英雄》电影观后感.docx

-

0Hnsjy大学英语四级真题听力原文.docx

-

02冬期雨期施工措施.docx

-

3安徽理工大学人人大使团.docx

-

5 外币业务会计处理 练习.docx

-

07年下学期教师法制学习资料.docx

-

09货币政策.docx

-

10第九章 会议礼仪.docx

-

12温度与物态变化教学案讲解.docx

-

五年职业规划范文复习过程.docx

-

下半年人力资源管理师三级理论知识真题.docx

-

小班科学探索小水滴旅行记doc.docx

-

小学期中表彰大会校长讲话稿doc.docx

-

效用理论.docx

-

新教材人教版地理必修一第三章第二节海水的性质同步练习含答案.docx

-

徐汇区华泾镇地块项目策划书.docx

-

学校第28个爱国卫生月活动方案.docx

-

阳极氧化膜的电解着色.docx

-

一建工程经济计算公式汇总及计算题解析.docx

-

仪器仪表常用英语词汇.docx

-

英语浙江省丽水市英语中考真题.docx

-

有关竞争的事例.docx

-

云南茶叶产业发展的基本情况.docx

-

浙江专用高考英语大一轮新优化复习Unit3TheMillionPoundBankNote课件新人.docx

-

执业药师药事管理与法规检测试题1完整篇doc.docx

-

中国玉米产消量供需平衡情况玉米价格走势及市场演变进程分析.docx

-

中心学校与学校领导签订一岗双责责任书知识讲解.docx

-

注册共用设备工程师暖通专业知识点整理.docx