《计量经济学》实验报告.docx

《计量经济学》实验报告.docx

- 文档编号:4618181

- 上传时间:2023-05-07

- 格式:DOCX

- 页数:18

- 大小:25.59KB

《计量经济学》实验报告.docx

《《计量经济学》实验报告.docx》由会员分享,可在线阅读,更多相关《《计量经济学》实验报告.docx(18页珍藏版)》请在冰点文库上搜索。

《计量经济学》实验报告

计量经济学

实

验

报

告

学号1111111111

姓名xxx

专业班级软件1101班

指导老师xx

日期20xx年xx月

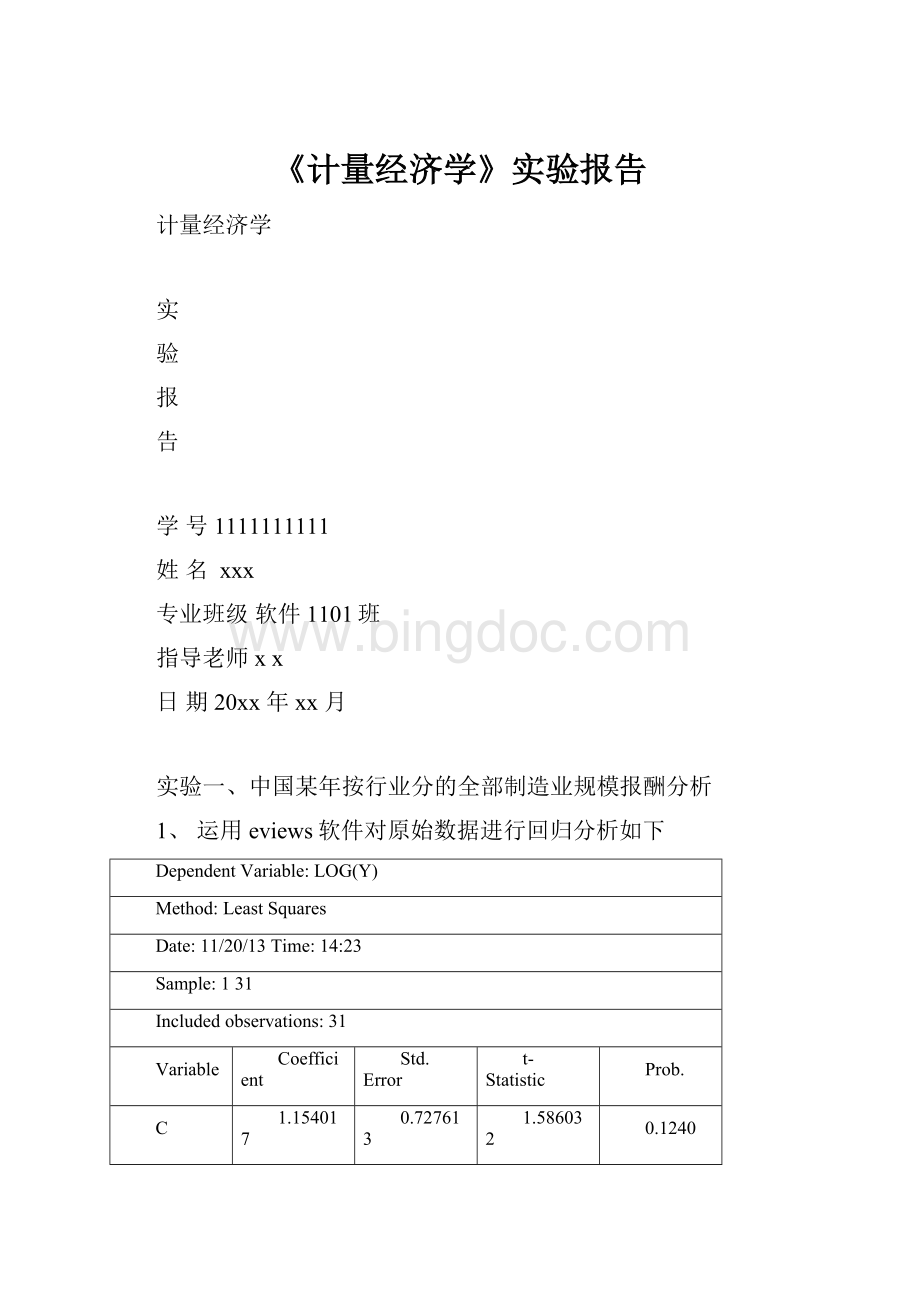

实验一、中国某年按行业分的全部制造业规模报酬分析

1、运用eviews软件对原始数据进行回归分析如下

DependentVariable:

LOG(Y)

Method:

LeastSquares

Date:

11/20/13Time:

14:

23

Sample:

131

Includedobservations:

31

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.154017

0.727613

1.586032

0.1240

LOG(K)

0.609232

0.176378

3.454120

0.0018

LOG(L)

0.360799

0.201592

1.789752

0.0843

R-squared

0.809924

Meandependentvar

7.494001

AdjustedR-squared

0.796347

S.D.dependentvar

0.942959

S.E.ofregression

0.425538

Akaikeinfocriterion

1.220842

Sumsquaredresid

5.070322

Schwarzcriterion

1.359615

Loglikelihood

-15.92306

F-statistic

59.65458

Durbin-Watsonstat

0.793198

Prob(F-statistic)

0.000000

2、参数检验模型估计

DependentVariable:

LOG(Y/L)

Method:

LeastSquares

Date:

11/20/13Time:

14:

30

Sample:

131

Includedobservations:

31

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.026065

0.596770

1.719365

0.0962

LOG(K/L)

0.608138

0.173590

3.503294

0.0015

R-squared

0.297363

Meandependentvar

3.100044

AdjustedR-squared

0.273134

S.D.dependentvar

0.491331

S.E.ofregression

0.418892

Akaikeinfocriterion

1.159931

Sumsquaredresid

5.088634

Schwarzcriterion

1.252447

Loglikelihood

-15.97894

F-statistic

12.27307

Durbin-Watsonstat

0.846451

Prob(F-statistic)

0.001511

实验二、某年中国部分城镇家庭平均可支配收入与消费性支出研究

1、利用eviews软件分析(图示法)

2、Eviews软件下载,OLS的估计结果如下

DependentVariable:

Y

Method:

LeastSquares

Date:

11/20/13Time:

14:

39

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

272.3635

159.6773

1.705713

0.1053

X

0.755125

0.023316

32.38690

0.0000

R-squared

0.983129

Meandependentvar

5199.514

AdjustedR-squared

0.982192

S.D.dependentvar

1625.275

S.E.ofregression

216.8900

Akaikeinfocriterion

13.69130

Sumsquaredresid

846743.0

Schwarzcriterion

13.79087

Loglikelihood

-134.9130

F-statistic

1048.912

Durbin-Watsonstat

1.670234

Prob(F-statistic)

0.000000

3、异方差检验

a、首先进行GQ检验:

对X从大到小排列,却掉中间4个,对前后两个样本进行OLS估计,样本容量为8.

前一个样本的OLS估计结果如下

DependentVariable:

Y

Method:

LeastSquares

Date:

11/20/13Time:

14:

45

Sample:

18

Includedobservations:

8

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1277.161

1540.604

0.829000

0.4388

X

0.554126

0.311432

1.779287

0.1255

R-squared

0.345397

Meandependentvar

4016.814

AdjustedR-squared

0.236296

S.D.dependentvar

166.1712

S.E.ofregression

145.2172

Akaikeinfocriterion

13.00666

Sumsquaredresid

126528.3

Schwarzcriterion

13.02652

Loglikelihood

-50.02663

F-statistic

3.165861

Durbin-Watsonstat

3.004532

Prob(F-statistic)

0.125501

后一个样本的OLS估计结果如下

DependentVariable:

Y

Method:

LeastSquares

Date:

11/20/13Time:

14:

50

Sample:

1320

Includedobservations:

8

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

212.2118

530.8892

0.399729

0.7032

X

0.761893

0.060348

12.62505

0.0000

R-squared

0.963723

Meandependentvar

6760.477

AdjustedR-squared

0.957676

S.D.dependentvar

1556.814

S.E.ofregression

320.2790

Akaikeinfocriterion

14.58858

Sumsquaredresid

615472.0

Schwarzcriterion

14.60844

Loglikelihood

-56.35432

F-statistic

159.3919

Durbin-Watsonstat

1.722960

Prob(F-statistic)

0.000015

b、怀特检验

WhiteHeteroskedasticityTest:

F-statistic

14.63595

Probability

0.000201

Obs*R-squared

12.65213

Probability

0.001789

TestEquation:

DependentVariable:

RESID^2

Method:

LeastSquares

Date:

11/20/13Time:

14:

56

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-180998.9

103318.2

-1.751858

0.0978

X

49.42846

28.93929

1.708006

0.1058

X^2

-0.002115

0.001847

-1.144742

0.2682

R-squared

0.632606

Meandependentvar

42337.15

AdjustedR-squared

0.589384

S.D.dependentvar

45279.67

S.E.ofregression

29014.92

Akaikeinfocriterion

23.52649

Sumsquaredresid

1.43E+10

Schwarzcriterion

23.67585

Loglikelihood

-232.2649

F-statistic

14.63595

Durbin-Watsonstat

2.081758

Prob(F-statistic)

0.000201

C、采用稳健标准误的方法修正原OLS的标准差

DependentVariable:

Y

Method:

LeastSquares

Date:

11/20/13Time:

15:

13

Sample:

120

Includedobservations:

20

WhiteHeteroskedasticity-ConsistentStandardErrors&Covariance

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

272.3635

181.6757

1.499174

0.1512

X

0.755125

0.031636

23.86886

0.0000

R-squared

0.983129

Meandependentvar

5199.515

AdjustedR-squared

0.982192

S.D.dependentvar

1625.275

S.E.ofregression

216.8900

Akaikeinfocriterion

13.69130

Sumsquaredresid

846743.0

Schwarzcriterion

13.79087

Loglikelihood

-134.9130

F-statistic

1048.912

Durbin-Watsonstat

2.087986

Prob(F-statistic)

0.000000

实验三、社会固定资产投资总额与工业增加值的研究

1、在eviews软件下,用图示法表示

3、利用eviews软件,得出如图的回归结果

DependentVariable:

LOG(Y)

Method:

LeastSquares

Date:

11/20/13Time:

15:

24

Sample:

19802007

Includedobservations:

28

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.588478

0.134220

11.83492

0.0000

LOG(X)

0.854415

0.014219

60.09058

0.0000

R-squared

0.992851

Meandependentvar

9.552256

AdjustedR-squared

0.992576

S.D.dependentvar

1.303948

S.E.ofregression

0.112351

Akaikeinfocriterion

-1.465625

Sumsquaredresid

0.328192

Schwarzcriterion

-1.370468

Loglikelihood

22.51876

F-statistic

3610.878

Durbin-Watsonstat

0.379323

Prob(F-statistic)

0.000000

3、利用eviews软件,通过LM检验法进行检验

Breusch-GodfreySerialCorrelationLMTest:

F-statistic

32.78471

Probability

0.000006

Obs*R-squared

15.88607

Probability

0.000067

TestEquation:

DependentVariable:

RESID

Method:

LeastSquares

Date:

11/20/13Time:

15:

32

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.023345

0.090124

0.259033

0.7977

LOG(X)

-0.002836

0.009551

-0.296927

0.7690

RESID(-1)

0.769716

0.134430

5.725793

0.0000

R-squared

0.567360

Meandependentvar

-5.76E-16

AdjustedR-squared

0.532748

S.D.dependentvar

0.110251

S.E.ofregression

0.075363

Akaikeinfocriterion

-2.232045

Sumsquaredresid

0.141989

Schwarzcriterion

-2.089309

Loglikelihood

34.24863

F-statistic

16.39235

Durbin-Watsonstat

1.042286

Prob(F-statistic)

0.000028

2阶检验

Breusch-GodfreySerialCorrelationLMTest:

F-statistic

23.23224

Probability

0.000002

Obs*R-squared

18.46328

Probability

0.000098

TestEquation:

DependentVariable:

RESID

Method:

LeastSquares

Date:

11/20/13Time:

15:

45

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.000108

0.082122

0.001316

0.9990

LOG(X)

-0.000134

0.008713

-0.015411

0.9878

RESID(-1)

1.115701

0.182417

6.116202

0.0000

RESID(-2)

-0.473435

0.185900

-2.546719

0.0177

R-squared

0.659403

Meandependentvar

-5.76E-16

AdjustedR-squared

0.616828

S.D.dependentvar

0.110251

S.E.ofregression

0.068246

Akaikeinfocriterion

-2.399823

Sumsquaredresid

0.111781

Schwarzcriterion

-2.209508

Loglikelihood

37.59752

F-statistic

15.48816

Durbin-Watsonstat

1.590500

Prob(F-statistic)

0.000008

3阶检验

Breusch-GodfreySerialCorrelationLMTest:

F-statistic

14.97751

Probability

0.000013

Obs*R-squared

18.52001

Probability

0.000344

TestEquation:

DependentVariable:

RESID

Method:

LeastSquares

Date:

11/20/13Time:

15:

54

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.004190

0.084359

0.049669

0.9608

LOG(X)

-0.000605

0.008965

-0.067492

0.9468

RESID(-1)

1.152317

0.210377

5.477401

0.0000

RESID(-2)

-0.558721

0.297820

-1.876033

0.0734

RESID(-3)

0.079894

0.215356

0.370984

0.7140

R-squared

0.661429

Meandependentvar

-5.76E-16

AdjustedR-squared

0.602547

S.D.dependentvar

0.110251

S.E.ofregression

0.069506

Akaikeinfocriterion

-2.334361

Sumsquaredresid

0.111117

Schwarzcriterion

-2.096467

Loglikelihood

37.68105

F-statistic

11.23313

Durbin-Watsonstat

1.637381

Prob(F-statistic)

0.000034

4、引入自回归,eviews软件下,进行回归分析

DependentVariable:

LOG(Y)

Method:

LeastSquares

Date:

11/20/13Time:

16:

07

Sample(adjusted):

19822007

Includedobservations:

26afteradjustingendpoints

Convergenceachievedafter6iterations

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.462393

0.220284

6.638684

0.0000

LOG(X)

0.865727

0.022738

38.07363

0.0000

AR

(1)

1.153081

0.179485

6.424377

0.0000

AR

(2)

-0.516675

0.168866

-3.059681

0.0057

R-squared

0.998087

Meandependentvar

9.701508

AdjustedR-squared

0.997826

S.D.dependentvar

1.229613

S.E.ofregression

0.057334

Akaikeinfocriterion

-2.739210

Sumsquaredresid

0.072318

Schwarzcriterion

-2.545657

Loglikelihood

39.60973

F-statistic

3825.609

Durbin-Watsonstat

1.819675

Prob(F-statistic)

0.000000

InvertedARRoots

.58+.43i

.58-.43i

5、运用eviews软件Lm检验已没有序列相关性

Breusch-GodfreySerialCorrelationLMTest:

F-statistic

0.091157

Probability

0.765681

Obs*R-squared

0.112373

Probability

0.737458

实验四、家庭消费支出与可支配收入和个人财富的研究

1、在eviews软件中,可得如下回归结果

DependentVariable:

Y

Method:

LeastSquares

Date:

11/20/13Time:

16:

12

Sample:

110

Includedobservations:

10

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

245.5158

69.52348

3.531408

0.0096

X1

0.568425

0.716098

0.793781

0.4534

X2

-0.005833

0.070294

-0.082975

0.9362

R-squared

0.962099

Meandependentvar

1110.000

AdjustedR-squared

0.951270

S.D.dependentvar

314.2893

S.E.ofregression

69.37901

Akaikeinfocriterion

11.56037

Sumsquaredresid

33694.13

Schwarzcriterion

11.65115

Loglikelihood

-54.80185

F-statistic

88.84545

Durbin-Watsonstat

2.708154

Pr

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- 计量经济学 计量 经济学 实验 报告

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

《篮球行进间单手低手投篮》教学设计.docx

《篮球行进间单手低手投篮》教学设计.docx

-

《饲料添加剂管理条例》知识竞赛试题及答案要点.docx

-

4 物理届高三上学期第一次月考物理试题.docx

-

08第二学期研究生英语.docx

-

31氧气的性质与用途个案教学设计.docx

-

0225变电安规二次题库474道.docx

-

1992年大学英语四级.docx

-

Arts 专项练习.docx

-

《两只鸟蛋》说课稿.docx

-

《孙权劝学》选择阅读带答案.docx

-

《在操场上》教学反思.docx

-

4VMware FT容错原理与配置详解.docx

-

8套专升本艺术概论试题.docx

-

17秋学期《食品安全与日常饮食尔雅》在线作业2.docx

-

3500词汇40篇文章.docx

-

AST中央企业班组长岗位管理能力资格认证三期模拟10300009.docx

-

GMC大赛手册中文版.docx

-

JAVELIN智能球机.docx

-

P1口语重点题型素材更新版.docx

-

QMS质量管理体系审核员真题精选.docx

-

U2t2学教设计.docx

-

XX公路施工组织设计建议书.docx

-

XX省XX县治安拘留所工程建设项目可行性研究报告.docx

-

yy政治知识汇总架构.docx

-

安全生产违法行为行政处罚汇编.docx

-

百度网站的商业运营模式和盈利模式分析.docx

-

保险经营管理重点.docx

-

北极星群和山东群倾情奉献高考题解析5重庆卷.docx

-

《内科学》教学大纲.docx

-

《小学生数学报》全册苏教版六年级下.docx

-

5湖北省三类人员电工试题.docx

-

10食品经营过程与控制制度.docx

-

88页中考词汇表.docx

-

APACHEII评分.docx

-

17年高考语文全国卷1.docx

-

361度的年度策划.docx

-

C++循环结构23道题含答案共16页.docx

-

20XX临床医学自我鉴定3篇.docx

-

1208工作面风巷观测分析新改简洁.docx

-

DR技术参数及要求.docx

-

80首小学必背古诗词赏析1.docx

-

2608中级财务会计二期末复习要求的说明.docx

-

ENLOGIC智能PDU智能排插数据中心的安全卫士.docx

-

API6D24版标准评审表.docx

-

FreeNAS安装与应用应用篇 iSCSI的使用.docx

-

00179谈判与推销技巧简答.docx

-

GTJ基础主梁的计算学习.docx

-

360度考核体系和表单.docx

-

gb 11551乘用车正面碰撞的乘员保护doc.docx

-

icu护理常规重症医学科专科护理常规大学论文.docx

-

HEIDENHAIN五坐标编程CHAP19.docx