ch02.docx

ch02.docx

- 文档编号:13321604

- 上传时间:2023-06-13

- 格式:DOCX

- 页数:53

- 大小:49.79KB

ch02.docx

《ch02.docx》由会员分享,可在线阅读,更多相关《ch02.docx(53页珍藏版)》请在冰点文库上搜索。

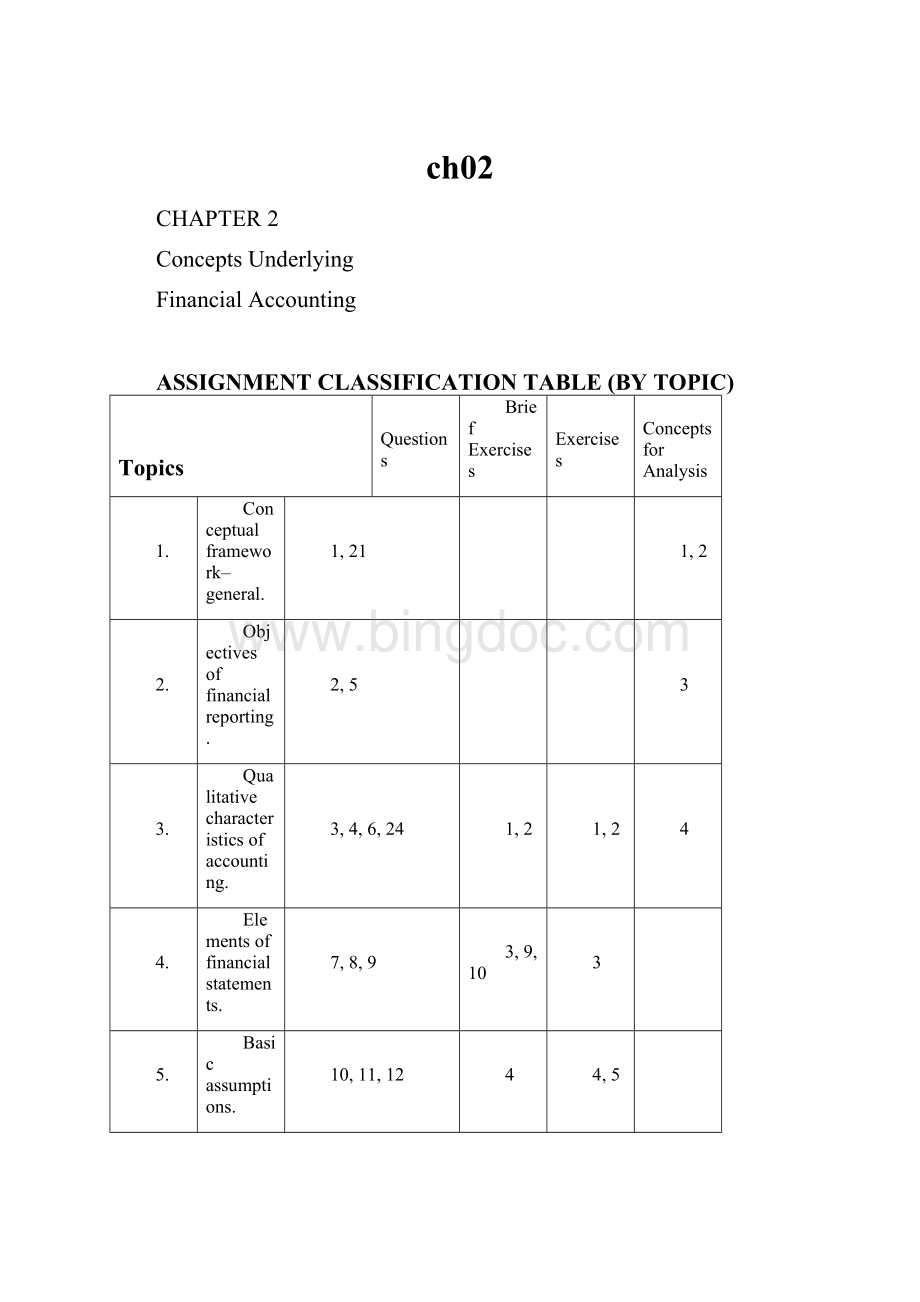

ch02

CHAPTER2

ConceptsUnderlying

FinancialAccounting

ASSIGNMENTCLASSIFICATIONTABLE(BYTOPIC)

Topics

Questions

BriefExercises

Exercises

Concepts

forAnalysis

1.

Conceptualframework–general.

1,21

1,2

2.

Objectivesoffinancialreporting.

2,5

3

3.

Qualitativecharacteristicsofaccounting.

3,4,6,24

1,2

1,2

4

4.

Elementsoffinancialstatements.

7,8,9

3,9,10

3

5.

Basicassumptions.

10,11,12

4

4,5

6.

Basicprinciples:

a.Historicalcost.

b.Revenuerecognition.

c.Expensematching.

d.Fulldisclosure.

13,14,15

16,17,18

19

20,21,22

5

4,5

5

4,5

4,5,6

5,6

5,6,7,8,9,10,11

7.

Accountingprinciples–comprehensive.

7,8

8.

Constraints.

23,24,25,26

6,7

1

12

9.

Comprehensiveassign-

mentsonassumptions,principles,andconstraints.

8

4,5

ASSIGNMENTCLASSIFICATIONTABLE(BYLEARNINGOBJECTIVE)

LearningObjectives

BriefExercises

Exercises

1.Describetheusefulnessofaconceptualframework.

2.DescribetheFASB’seffortstoconstructaconceptualframework.

3.Understandtheobjectivesoffinancialreporting.

4.Identifythequalitativecharacteristicsofaccountinginformation.

1,2

1,2

5.Describethebasicelementsoffinancialstatements.

3,10

3

6.Describethebasicassumptionsofaccounting.

4,8,9

4,5

7.Explaintheapplicationofthebasicprinciplesofaccounting.

5,9

4,5,6,7,8

8.Describetheimpactthatconstraintshaveonreportingaccountinginformation.

6,7,9

1,4,5

ASSIGNMENTCHARACTERISTICSTABLE

Item

Description

LevelofDifficulty

Time

(minutes)

E2-1

Qualitativecharacteristics.

Moderate

25–30

E2-2

Qualitativecharacteristics.

Simple

15–20

E2-3

Elementsoffinancialstatements.

Simple

15–20

E2-4

Assumptions,principles,andconstraints.

Simple

15–20

E2-5

Assumptions,principles,andconstraints.

Moderate

20–25

E2-6

Fulldisclosureprinciple.

Complex

20–25

E2-7

Accountingprinciples–comprehensive.

Moderate

20–25

E2-8

Accountingprinciples–comprehensive.

Moderate

20–25

CA2-1

Conceptualframework–general.

Simple

20–25

CA2-2

Conceptualframework–general.

Simple

25–35

CA2-3

Objectivesoffinancialreporting.

Moderate

25–35

CA2-4

Qualitativecharacteristics.

Moderate

30–35

CA2-5

Revenuerecognitionandmatchingprinciple.

Complex

25–30

CA2-6

Revenuerecognitionandmatchingprinciple.

Moderate

30–35

CA2-7

Matchingprinciple.

Complex

20–25

CA2-8

Matchingprinciple.

Moderate

20–25

CA2-9

Matchingprinciple.

Moderate

20–30

CA2-10

Qualitativecharacteristics.

Moderate

20–30

CA2-11

Matching–ethics

Moderate

20–25

CA2-12

Cost/Benefit

Moderate

30–35

ANSWERSTOQUESTIONS

1.Aconceptualframeworkisacoherentsystemofinterrelatedobjectivesandfundamentalsthatcanleadtoconsistentstandardsandthatprescribesthenature,function,andlimitsoffinancialaccountingandfinancialstatements.Aconceptualframeworkisnecessaryinfinancialaccountingforthefollowingreasons:

1.ItwillenabletheFASBtoissuemoreusefulandconsistentstandardsinthefuture.

2.Newissueswillbemorequicklysolublebyreferencetoanexistingframeworkofbasictheory.

3.Itwillincreasefinancialstatementusers’understandingofandconfidenceinfinancialreporting.

4.Itwillenhancecomparabilityamongcompanies’financialstatements.

2.Theprimaryobjectivesoffinancialreportingareasfollows:

1.Provideinformationusefulininvestmentandcreditdecisionsforindividualswhohaveareasonableunderstandingofbusiness.

2.Provideinformationusefulinassessingfuturecashflows.

3.Provideinformationaboutenterpriseresources,claimstotheseresources,andchangesinthem.

3.“Qualitativecharacteristicsofaccountinginformation”arethosecharacteristicswhichcontributetothequalityorvalueoftheinformation.Theoverridingqualitativecharacteristicofaccountinginformationisusefulnessfordecisionmaking.

4.Relevanceandreliabilityarethetwoprimaryqualitiesofusefulaccountinginformation.Forinforma-tiontoberelevant,itshouldhavepredictivevalueorfeedbackvalue,anditmustbepresentedonatimelybasis.Relevantinformationhasabearingonadecisionandiscapableofmakingadifferenceinthedecision.Relevantinformationhelpsuserstomakepredictionsabouttheoutcomesofpast,present,andfutureevents,ortoconfirmorcorrectpriorexpectations.Reliableinformationcanbedependedupontorepresenttheconditionsandeventsthatitisintendedtorepresent.Reliabilitystemsfromrepresentationalfaithfulness,neutrality,andverifiability.

5.Inprovidinginformationtousersoffinancialstatements,theBoardreliesongeneral-purposefinancialstatements.Theintentofsuchstatementsistoprovidethemostusefulinformationpossibleatminimalcosttovarioususergroups.Underlyingtheseobjectivesisthenotionthatusersneedreasonableknowledgeofbusinessandfinancialaccountingmatterstounderstand

theinformationcontainedinfinancialstatements.Thispointisimportant:

itmeansthatinthepreparationoffinancialstatementsalevelofreasonablecompetencecanbeassumed;thishasanimpactonthewayandtheextenttowhichinformationisreported.

6.Comparabilityfacilitatescomparisonsbetweeninformationabouttwodifferententerprisesataparticularpointintime.Consistencyfacilitatescomparisonsbetweeninformationaboutthesameenterpriseattwodifferentpointsintime.

7.Atpresent,theaccountingliteraturecontainsmanytermsthathavepeculiarandspecificmeanings.Someofthesetermshavebeeninuseforalongperiodoftime,andtheirmeaningshavechangedovertime.Sincetheelementsoffinancialstatementsarethebuildingblockswithwhichthestatementsareconstructed,itisnecessarytodevelopabasicdefinitionalframeworkforthem.

8.Distributionstoownersdifferfromexpensesandlossesinthattheyrepresenttransferstoowners,andtheydonotarisefromactivitiesintendedtoproduceincome.Expensesdifferfromlossesinthattheyarisefromtheentity’songoingmajororcentraloperations.Lossesarisefromperipheralorincidentaltransactions.

QuestionsChapter2(Continued)

9.Investmentsbyownersdifferfromrevenuesandgainsinthattheyrepresenttransfersbyownerstotheentity,andtheydonotarisefromactivitiesintendedtoproduceincome.Revenuesdifferfromgainsinthattheyarisefromtheentity’songoingmajororcentraloperations.Gainsarisefromperipheralorincidentaltransactions.

10.Thefourbasicassumptionsthatunderliethefinancialaccountingstructureare:

1.Aneconomicentityassumption.

2.Agoingconcernassumption.

3.Amonetaryunitassumption.

4.Aperiodicityassumption.

11.(a)Inaccountingitisgenerallyagreedthatanymeasuresofthesuccessofanenterpriseforperiodslessthanitstotallifeareatbestprovisionalinnatureandsubjecttocorrection.Measurementofprogressandstatusforarbitrarytimeperiodsisapracticalnecessitytoservethosewhomustmakedecisions.Itisnottheresultofpostulatingspecifictimeperiodsasmeasurablesegmentsoftotallife.

(b)Thepracticeofperiodicmeasurementhasledtomanyofthemostdifficultaccountingproblemssuchasinventorypricing,depreciationoflong-termassets,andthenecessityforrevenuerecognitiontests.Theaccrualsystemcallsforassociatingrelatedrevenuesandexpenses.Thisbecomesverydifficultforanarbitrarytimeperiodwithincompletetransactionsinprocessatboththebeginningandtheendoftheperiod.Anumberofaccountingpracticessuchasadjustingentriesorthereportingofcorrectionsofpriorperiodsresultdirectlyfromeffortstomakeeachperiod’scalculationsasaccurateaspossibleandyetrecognizingthattheyareonlyprovisionalinnature.

12.Themonetaryunitassumptionassumesthattheunitofmeasure(thedollar)remainsreasonablystablesothatdollarsofdifferentyearscanbeaddedwithoutanyadjustment.Whenthevalueofthedollarfluctuatesgreatlyovertime,themonetaryunitassumptionlosesitsvalidity.

TheFASBinConceptNo.5indicatedthatitexpectsthedollarunadjustedforinflationordeflationtobeusedtomeasureitemsrecognizedinfinancialstatements.OnlyifcircumstanceschangedramaticallywilltheBoardconsideramorestablemeasurementunit.

13.Someoftheargumentswhichmightbeusedareoutlinedbelow:

1.Costisdefiniteandreliable;othervalueswouldhavetobedeterminedsomewhatarbitrarilyandtherewouldbeconsiderabledisagreementastotheamountstobeused.

2.Amountsdeterminedbyotherbaseswouldhavetoberevisedfrequently.

3.Comparisonwithothercompaniesisaidedifcostisemployed.

4.Thecostsofobtainingreplacementvaluescouldoutweighthebenefitsderived.

14.Revenueisgenerallyrecognizedwhen

(1)realizedorrealizable,and

(2)earned.

Theadoptionofthesalebasisistheaccountant’spracticalsolutiontotheextremelydifficultproblemofmeasuringrevenueunderconditionsofuncertaintyastothefuture.Therevenueisequaltotheamountofcashthatwillbereceivedduetotheoperationsofthecurrentaccountingperiod,butthisamountwillnotbedefinitelyknownuntilsuchcashiscollected.Theaccountant,underthesecircumstances,insistsonhaving“objectiveevidence,”thatis,evidenceexternaltothefirmitself,onwhichtobaseanestimateoftheamountofcashthatwillbereceived.Thesaleisconsideredtobetheearliestpointatwhichthisevidenceisavailableintheusualcase.Untilthesaleismade,anyestimateofthevalueof

- 配套讲稿:

如PPT文件的首页显示word图标,表示该PPT已包含配套word讲稿。双击word图标可打开word文档。

- 特殊限制:

部分文档作品中含有的国旗、国徽等图片,仅作为作品整体效果示例展示,禁止商用。设计者仅对作品中独创性部分享有著作权。

- 关 键 词:

- ch02

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

冰点文库所有资源均是用户自行上传分享,仅供网友学习交流,未经上传用户书面授权,请勿作他用。

#电控发动机的故障诊断与排除.docx

#电控发动机的故障诊断与排除.docx

-

《财务管理学》人大版第五章习题答案.docx

-

《公路养护工程量清单及计量规范》编制.docx

-

《反抗之真心英雄》读后感.docx

-

《C语言程序设计》阅读程序写结果试题汇总.docx

-

《汉书艺文志》小说家与子部小说著录.docx

-

《江苏省建设工程施工项目经理部和项目监理机构主要管理人员配备办法》.docx

-

《C语言程序设计》课程形成性考核作业.docx

-

《诚实与信任》教学设计.docx

-

《变化社会中的政治秩序》读后感.docx

-

《44光的折射》教案.docx

-

《归去来兮辞》优化教案及课文解析.docx

-

《大数据导论》19秋期末考核0001.docx

-

《大型养路机械使用管理规则》.docx

-

《混凝土结构工程施工质量验收规范》GB 条文说明.docx

-

《会计基础》练习答案解析.docx

-

《民法典》试题第三编合同二试题及答案.docx

-

《建设工程消防监督管理规定》公安部119号令1101.docx

-

《赢》杰克韦尔奇读书笔记.docx

-

《活出全新的自己》读后感精选9篇.docx

-

《拿破仑传》读后感范文5篇.docx

-

《去年的树》课堂实录及点评doc.docx

-

《人体解剖生理学》练习题库.docx

-

00以内整数加减.docx

-

《手工制作中培养幼儿创意能力的实践研究》完整.docx

-

《校园防汛工作计划》.docx

-

06年批发零售业研究报告.docx

-

《小王子》金句赏析英语作文.docx

-

《中华人民共和国职业病防治法》条文释义下.docx

-

007电子请柬.docx

-

1物业事业部运营管理方案.docx

-

《新闻写作教程》中篇整理资料.docx

-

人教版品德与社会小学四年级上册全册教案文档格式.docx

-

人教版四年级数学下册乘除法简便计算 607Word文档格式.docx

-

陕旅版小学英语六年级下册期末测试题Word格式文档下载.doc

-

人教版小学语文三年级下册第二单元练习题Word下载.docx

-

人教高中英语必修五知识点汇总Word格式文档下载.docx

-

仁爱英语中招模拟试题Word文件下载.docx

-

入股合伙合同范本合伙合同Word文件下载.docx

-

三级模拟试题19页文档格式.docx

-

上海牛津版英语小学六年级时态练习题Word文档格式.doc

-

山东临清市四所高中高二化学教学设计 选修5 第4章 第3节 蛋白质和核酸新人教选修5Word格式.docx

-

上海牛津英语6b预备年级英语期中模拟文档格式.doc

-

上海牛津英语四年级英语下期中复习题文档格式.doc

-

上海市闵行区2015学年第一学期六年级英语学科期末考试试卷(含答案)Word下载.doc

-

上海杉达学院关于教师和其他专业技术职务评聘实施办法Word文档下载推荐.docx

-

上消化道出血教案Word文档格式.docx

-

社团部门工作计划分析精选多篇Word格式文档下载.docx

-

深圳市房屋租赁合同书新版Word文档格式.docx

-

生产设备台帐文档格式.docx

-

草房子读书笔记1000字左右.docx